When deciding to take a loan, you must consider that various lenders have different variables regarding the loans. However, there are some general properties that most lenders consider before approving the loan.

Experts from title loans in San Antonio have provided us with the answers to our questions to help you manage your financial urges and get the needed loan.

Loan Cheetah

To boost your chance of getting the required loan, it’s useful to know what exactly lenders consider deciding factors for your loan. With such knowledge, you will be able to apply for your loan more confident that you will get the approval and resolve your financial occurrences.

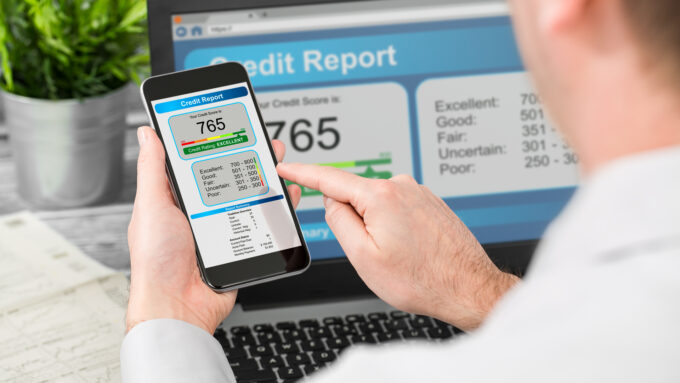

Your credit history

Credit is often the most significant aspect that lenders consider when reviewing your loan application. Having credit provides lenders with information that you have a financial record about your income, expenditures, transactions, payments, previous or current borrowings, and other related data. Also, this gives them a perception of how you are managing borrowed money.

Your credit report depicts and contains your credit score that reflects your creditworthiness. Credit reports are often generated by financial institutions such as credit reference bureaus or other financial administrations that can keep track of and collect data on the financial flow of business organizations and individuals with credit histories.

This information lenders find very valuable, especially if you had a borrowing in the past that you have paid off without defaulting and delaying payments; your chances to get a loan are significantly greater, contrary to those with poor credit history, which lenders consider as the rising risk of default.

Even though a higher credit score provides a stronger chance for approval than a low credit score, lenders don’t necessarily disclose the borrowers with a minimum credit score since the loan approval evaluation considers numerous factors, and credit score is just one of them.

However, lenders might demand different credit scores from different loanees. For instance, for some small business loans, lenders can require a higher credit score for insurance.

Capital

Lenders will consider if you have invested capital in the business and be more confident in giving the loan when you have insider ownership, preferably larger than the loan amount. They rely on the fact that you will not risk losing your investment and, by that, not losing theirs.

On the other hand, if you haven’t invested in your business before applying for loans, most lenders will take this as a precautionary signal, fearing that you won’t put enough effort into returning the business loan and investment.

Income and employment

If you are applying for a personal loan, lenders will consider your income and employment. Based on the amount of loan you intend to borrow, the lenders will require a higher income to be more confident that you will be able to pay back the loan.

Also, they will typically request steady employment. Generally, lenders will want to be sure that you are able to return the loan by counting on consistent and sufficient income.

Self-employed persons or individuals with part-year jobs will have fewer chances to get loan approval than those with years of employment in established companies.

Additionally, lenders will consider the debt-to-income ratio, which considers your monthly account obligations expressed as a percentage of your monthly income. Most lenders don’t accept a debt-to-income ratio greater than 43%.

Business plan

If you are eager to apply for a business loan, one thing is crucial – have a business plan. This is due to lenders’ awareness that your power to repay the loan mostly depends on your business profit.

Therefore, if you have a clear and potentially solvent business plan, lenders will be more secure in approving you a loan, assuming that you will be capable of returning the borrowing. Wherever you attempt to get the loan, lenders will want to know what you will do to ensure loan repayment; for this reason, lenders are more willing to approve the loan if you provide them with your business plan.

Another aspect that leaders usually consider is the current performance of your business. Besides the business plan that reflects the reasonable possibility of working out successfully, lenders prefer a business that is not in a desperate situation and requires the resources to grow instead of surviving.

On that account, when creating a business plan, focus on the opportunities that your business will have with the loan as a financial injection that will boost your business instead of displaying the image of make or break a business.

Business skills

Even though the loanee has collateral to repay the loan, lenders often consider a person’s character in terms of capability to manage the loan and handle the business to make it profitable. In these terms, they evaluate loanees’ reputation and trustworthiness.

Collateral value

Collateral is considered the value loanee agrees to give to the lender in cases of inability to remain with paying loan installments. Loans with collateral are more secure for lenders than those without collateral.

Additionally, secured loans usually imply a lower interest rate. Further, the value of the collateral will determine the amount of your loan, meaning that you will be able to borrow a greater money amount if you have significant collateral. Lenders secure their loans this way, ensuring that they can get back their money in case the loanee is not able to pay the loan.

For example, the loan value you want to borrow for buying a house can’t exceed the value of the house since the house is a collateral the lender can take to recount its money.

Down payment

Some lenders can request a down payment that will determine the amount of your loan and interest rate. The more money you pay upfront, the less you will have to borrow. The fewer or no down payment sometimes means that you will pay more in interest.

However, many lenders don’t require any down payment, and this feature is more typical for bank loans.

Summary

The bottom line is that all of these factors might not be individually determinating for loan approval but together contributes to evaluation. Two people with the same credit score will not meet the same application outcome.

However, knowing the factors that are most valid in getting the loan will provide you with a comprehension of your chances of getting the loan you require and the opportunity to increase the likelihood of approval by improving your facets.